Here are some important frequently asked questions about the change from COSO 1992 to COSO 2013 and what this could mean to your company.

Jump to the topic you are looking for: |

|

|

|

1. What is COSO 2013?COSO 1992 has been the most widely adopted internal control framework used since the passage of the Sarbanes-Oxley Act of 2002. COSO 2013 is an update to the 1992 version. COSO 2013 is:

|

|

|

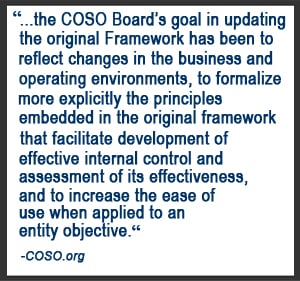

2. Why has COSO changed?The intention of the COSO 2013 edition is to:

|

|

|

3. How do I know if COSO 2013 applies to me?This change applies to all public companies traded on the US exchanges and any company trying to maintain compliance with the Sarbanes-Oxley Act of 2002. |

|

|

4. I am a non-accelerated filer so this doesn't apply to me, right?WRONG! If your company is required to attest to Section 404(a) compliance typically via your 10-Q Item 4, 10-K Item 9, 302, or 906 certifications (so all public companies of any size), this change applies to you. |

|

|

5. What changes should I expect?Some changes include:

|

|

|

6. When is the due date?Adoption of the new standards must be demonstrated by your next fiscal year-end after December 15, 2014. This means if you are a calendar year-end filer, then you must demonstrate compliance by 12/31/2014. |

|

|

7. What is the best approach to adopting COSO 2013?The change will require a reassessment of your current control environment by people familiar with the COSO 2013 requirements to determine how much work is needed to bring your internal control infrastructure up to the new standards. We recommend starting this work as early in 2014 as possible since the changes are substantial. This change will be different for each company but we have a strategy to get you through this process very quickly. |

|

|

8. Why should I talk to Vibato about COSO 2013?Vibato has created a complete COSO 2013 Made Simple to help complete the transition in an efficient and effective manner. We would be happy to speak with you about where you are now and what you will need to do to demonstrate compliance with the new requirements. Please call us at 1-888-4-VIBATO, 415.240.4867, or email us by clicking this link: COSO 2013 Inquiry. |

|

|

9. I'm an external auditor looking for information.We hold regular web-based training's on available via our Webinars page. We also offer on site training and technology licensing options. Please call 1-888-4-VIBATO or 415.240.4867 for more information. CPE is available for all training options. |

|

|

10. How should I get started?

|

|

|

11. "Help me understand what I'm in for..."First, know it will be all right. You've come to the right place. We have pre-drafted controls - by process - that meet the new COSO 2013 compliance requirements. Typically, in less than 1 day, we can assess your current controls against the new COSO 2013 control requirements and provide you with a detailed list of what you’ll need to change to meet the new requirements. Additionally, we have ready-to-use accounting templates (ex. policies, procedures, forms, spreadsheets, etc.) already prepared to show you exactly what you need to do to execute the new COSO 2013 controls. You may use these as a replacement for your current documents or you may use these as a guide and training materials. Now, register to your right to start your complimentary assessment of your current internal control structure to learn what the change to COSO 2013 may require for your company. |

|

|

Will the SEC's financial reporting requirements change because of COSO 2013?It appears that the SEC is in a wait and see mode right now: "I understand that COSO intends to supersede their 1992 Framework as of December 15, 2014, and we expect there will be questions about whether the SEC will provide management with any transition or implementation guidance to change from the existing framework to the new framework...SEC staff plans to monitor the transition for issuers using the 1992 framework to evaluate whether and if any staff or Commission actions become necessary or appropriate at some point in the future. However, at this time, I’ll simply refer users of the COSO framework to the statements COSO has made about their new framework and their thoughts about transition." - Paul Beswick, Chief Accountant, Office of the Chief Accountant, U.S. Securities and Exchange Commission, May 30, 2013" |